Written By David Kotter

Apartments in Phoenix are extremely popular right now and demand for them does not seem to be waning. The soaring interest in the Phoenix apartment market leaves potential investors with a few questions. Why is this happening? What are the specific areas that one should give attention to? Finally, how can you structure a deal so that you can win it and still maintain internal credit integrity?

Why is this happening?

We believe there are a couple of things that are driving the craze of apartments. First, you have a net migration reality taking place right now and a perception issue. According to the report on put out by North American moving services “Where are Americans Moving?” In 2019 the top 5 inbound states were Idaho, Arizona, South Carolina, Tennessee and North Carolina. Ironically, the top three states outbound were Illinois, California and New Jersey. According to an AZ Big Media report, the primary origin of newcomers to Arizona was from California. Ex-Californians accounted for 68,516. It is a fact that Californians are coming here in droves, and other areas as well.

The next item is perception. If you’re from California, you’re probably used to paying $250,000 to $500,000 per door for an apartment; insane! At some point, you’re actually paying to own the property. So, here comes the perception shift. One day you wake up and realize that you can drive five to six hours away and get the exact same deal for a half to a fourth of the price.

A California client recently asked me if he was overpaying for a property in Phoenix. My response was “yes you are”. He was quiet for a minute and responded saying “David, I don’t care because it is better to get in now before prices go up”. There, my friend, you have a complete perception change. As they say, one man’s trash is another man’s treasure.

What are the specific areas to focus on?

Key Takeaways From 2018

● Occupancy over the 12-month period at 92.3% in 1Q 2018 to 94.3% in 4Q 2018. Overall, occupancy averaged 95.07%.

● Rental rates PSF over the 12-month period at $1.07 PSF in 1Q 2018 to $1.11 PSF in 4Q 2018. Overall, rental rates have averaged $1.09 PSF.

● Rent growth over the 12-month period at 4.6% in 1Q 2018 to 5.0% in 4Q 2018. Overall, rent growth has averaged 4.63%.

● Cap rates over the 12-month period at 6.02% in 1Q 2018 to 5.96% in 4Q 2018. Overall, cap rates averaged 5.92%.

● Sale prices per unit have increased over the 12-month period from $89,092 per unit in Q1 2018 to $126,142 per unit in Q4 2018, or a whopping 41% increase in sale price PSF. The most significant sale in 2018 was Tides Arcadia, a 20-unit Class B/C apartment that sold for $315,000 per unit. The largest property to sell was Canyon 35, a 98-unit Class B/C apartment that sold for $83,168 per unit.

● Construction stats: In 2018, 11 Class A multifamily properties constructed (530 units) were delivered between 20-100 units.

So, what does this all mean for 2018?

In 2018, the market saw a decrease in vacancy, which directly affected the increase in rental rates. Rental rates increased 3.74% over from 1Q to 4Q, roughly 1% per quarter. Smaller properties between 25-50 are typically more desirable for investors as the cost of maintaining the properties is lower, and management fees can encompass the payroll costs.

Payroll costs, as many owners know, can be one of the more costly expenses on the balance sheet because of the demand for smaller property types, the attractiveness of a value-add investment, the trend of decreasing capitalization rates was evident by the compression seen from 1Q to 4Q. Additionally, because of the demand of owning smaller assets, sale prices reported a compound change of 9.32% over the 12-month period. With decreasing cap rates, increasing rents, and increasing sale prices, 2018 was on the train to continual growth into 2019.

Key Takeaways From 2019

● Occupancy over the 12-month period at 95.5% in 1Q 2019 to 94.4% in 4Q 2019. Overall, occupancy averaged 95.5%.

● Rental rates over the 12-month period at $1.12 PSF in 1Q 2019 to $1.15 PSF in 4Q 2019. Overall, rental rates have averaged $1.14 PSF.

● Rent growth over the 12-month period at 4.8% in 1Q 2019 to 4.3% in 4Q 2019. Overall, rent growth has averaged 4.68%.

● Cap rates over the 12-month period at 5.74% in 1Q 2019 to 5.55% in 4Q 2019. Overall, cap rates averaged 5.65%.

● Sale prices per unit remained steady over the 12-month period from $129,053 per unit in Q1 2019 to $126,405 per unit in Q4 2019, with an average sale price of $116,321 per unit. The most significant sale in 2019 was Union at Roosevelt, an 80-unit Class A apartment that was built in 2017 and sold for $337,500 per unit. The largest property to sell was Vibe on Thomas, a 100-unit Class B/C apartment that sold for $84,500 per unit as a value-add investment sale.

● Construction stats: In 2019, 11 Class A multifamily properties constructed (550 units) were delivered between 20-100 units.

So, what does this all mean for 2019?

The market in 2018 and 2019 saw a decrease in Phoenix apartment vacancy and an increase in rental rates. Rental rates increased by 4.29% over the 2018 year. The trend of decreasing capitalization rates continued as they went from an average of 5.92% in 2018 to 5.65% in 2019, a 27-basis point decrease. The appetite for apartment sales did not diminish in 2019. Sale prices reported averaged $116,321 per unit for units between 20-100 units. With decreasing cap rates, increasing rents, and increasing sale prices, 2020 was poised for another growth year. Or so we thought…

Now What … Going Forward?

The Coronavirus pandemic was an unexpected “black swan” event that economists could not have predicted. Using metrics from CoStar which uses Oxford Economics, forecasting is trended based on the current economic climate in the COVID era. “Base Case” scenario is a good representation of a “V-shaped recovery” and would be consistent with a positive outcome in the search for a vaccine that leads to a significant rebound in economic activity. “Moderate Upside” scenario is consistent with a successful near-full reopening of the US economy even prior to the development of a vaccine. “Moderate Downside” scenario is consistent with a very bad “W-shaped” recession and recovery which could be driven by a poor outcome with the coronavirus, where a vaccine is unable to be developed and the virus mutates enough every year that outbreaks are similar to the seasonal flu. Lastly, “Severe Downside” depicts a dire economic outcome, one that is comparable only to the Great Depression.

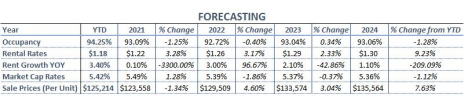

Using these forecast scenarios, we are able to determine base case forecasting for the next 5 years in the Phoenix MSA. Beginning in 2021, the following metrics have been forecasted:

As seen from the forecasting, Phoenix will fare well compared to other parts of the country. While an initial dip in Phoenix apartment occupancy and year-over-year rent growth is expected, sale prices and rental rates will continue to see an increase. Most underwriters and selling brokers are being conservative with rent growth projections in their pro formas and underwriting some higher concessions. This has been evident by the activity of sales in the Phoenix MSA, which in some cases turned to bidding wars. The forecasted concessions are a straight line and discussions with property owners determined that these smaller properties have not been offering concessions since occupancy has remained strong. Additionally, lenders are have not pulled back on financing proposed properties in the Phoenix MSA. There are currently 14 multifamily properties (1,063 units) under construction of 20-100 units or more in the Phoenix MSA. Another 25 properties are proposed (1,739 units). In the next 24 months, 47 multifamily properties will be delivered (3,289 units). By the end of 2020, 1,255 units will have been delivered in 17 different properties throughout the Phoenix MSA.

Bottom Line … How Do You Win?

All this information is great, but how do you apply this in real time to stay in the game of lending? Here are a few closing ideas:

1. Look heavily at localized information vs. regional. Every submarket can have a very different outcome. Larger data points can skew the reality of an area that might be doing great because of incomes, job growth, etc.

2. Talk to local property managers. The best people to tell you what is really going on are the people on the ground. Interview the property manager to gauge the temperature of the tenants and incoming prospect.

3. Ask the question “how can we vs. we can’t”. This question will open up many opportunities for structuring around risk. Maybe you take some reserves to pad against any future risk. Perhaps you can impound for some additional risks you see in the marketplace.

David Kotter serves as principal of Integrity Capital LLC, a limited liability company and commercial mortgage brokerage based in Scottsdale, Ariz. Kotter can be reached at (480) 219-1205. Arielle N. Litt is the Managing Director at BBG, Inc. – Phoenix and a certified general real estate appraiser. BBG, Inc is one of the nation’s largest real estate due diligence firms with more than 35 offices across the country serving more than 2,700 clients’ appraisal and third-party needs.

{kind=link}